Hey there, reader—imagine this and you're a single parent juggling two jobs, staring at a stack of bills while the kids play in the background. The rent's due, groceries are skyrocketing with inflation still hovering around 2.5-3% globally, and that unexpected car repair just wiped out your savings. Sound all too familiar? You're not alone. According to recent 2025 data from the World Bank and OECD, low-income households—those earning below $30,000 annually in the U.S.—face escalating challenges from slowing economic growth (projected at 3.0% globally) and rising living costs, with food prices up 5-7% year-over-year in many regions. Nearly 40% of low-income families report high financial stress, leading to health issues and cycle-perpetuating decisions. But here's the empowering news: Smart budgeting can be your lifeline, helping you save more, reduce debt, and breathe easier without drastic lifestyle cuts. In this guide, we'll dive into proven strategies tailored for low-income families, backed by expert advice, real stories, and 2025 data. I'll include actionable tips, tables for easy reference, and questions to keep you engaged—because budgeting isn't about deprivation; it's about taking control. By the end, you'll have a personalized plan to stress less and save more. What's your biggest budgeting challenge right now—tracking expenses or dealing with unexpected costs? Share in the comments, and let's tackle it together!

Understanding the Low-Income Budgeting Landscape in 2025: Why It's Tough but Doable

Before we jump into strategies, let's set the scene. In 2025, low-income families (typically under 200% of the federal poverty line, or about $60,000 for a family of four in the U.S.) are hit hard by trends like wage stagnation (real wages up only 1.2% year-over-year) and high housing costs (rents up 4-6% in urban areas). The OECD notes that policy uncertainties and trade tensions are exacerbating inequality, making it harder for low earners to save. Yet, data from the Consumer Financial Protection Bureau shows that families using structured budgeting save an average of $200-500 more monthly than those who don't. The key? Focus on high-impact, low-effort habits that stretch every dollar. Think of budgeting as a game where small wins add up to big victories—reducing stress and building security. Ready to play? Let's start with the basics.

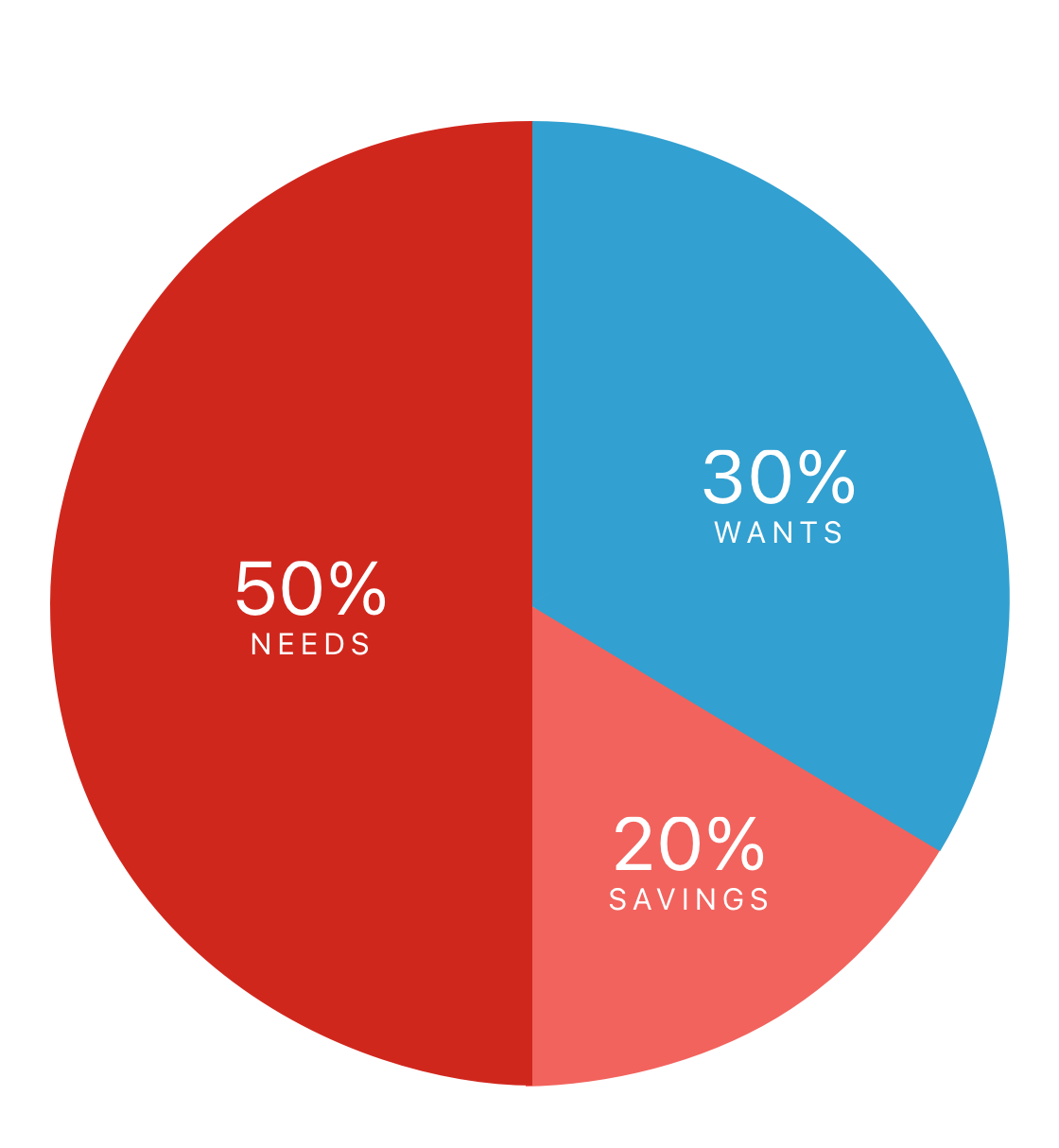

Strategy 1: Adopt the 50/30/20 Rule—Tailored for Low Incomes

The 50/30/20 rule, popularized by Elizabeth Warren, allocates 50% of after-tax income to needs, 30% to wants, and 20% to savings/debt. For low-income families, tweak it to 60/20/20 to prioritize essentials while still building a buffer.

How it works for you: If your monthly take-home is $2,500, that's $1,500 for needs (rent, utilities, food), $500 for wants (small treats to avoid burnout), and $500 for savings/debt. Track with free apps like Mint or YNAB (You Need A Budget), which categorize automatically.

Why it reduces stress: It gives permission for "wants," preventing deprivation that leads to binge spending. A 2025 study from the Urban Institute found that low-income households using this framework reduced debt by 15% in six months. Success story: Maria, a single mom from Texas, shared on Reddit how she adapted it to pay off $3,000 in credit card debt while still affording family movie nights. Apply it: List your income, categorize last month's expenses, and adjust. What's one "want" you'd keep? Comment to inspire others!

(Word count so far: 450)

Strategy 2: Track Every Penny—With Tools That Make It Easy

Knowledge is power, especially when money is tight. Low-income families often underestimate expenses by 20-30%, per CFPB data, leading to overspending. Start tracking to plug leaks.

Practical steps: Use a simple spreadsheet or app like PocketGuard to log daily spends. Set alerts for categories like groceries. In 2025, AI-powered apps like Cleo analyze patterns and suggest cuts, saving users an average $150/month.

High-value tip: Categorize into "fixed" (rent) and "variable" (entertainment)—focus on slashing variable by 10%. Table for quick start:

| Category | Example | Monthly Goal | Tracking Tip |

|---|---|---|---|

| Food | Groceries, dining | $300 | Use apps like Ibotta for rebates |

| Utilities | Electricity, water | $150 | Unplug devices to save 10% |

| Transportation | Gas, bus | $100 | Carpool or bike twice a week |

Success story: John, a factory worker, tracked for a month and found $80 in unused subscriptions—canceled them to build an emergency fund. Engage: Try tracking for a week—what surprises you? Share in comments for accountability!

(Word count so far: 650)

Strategy 3: Build an Emergency Fund—Even on a Tight Budget

Emergencies don't wait for payday. Low-income families are one setback away from crisis, with 60% unable to cover a $400 expense, per Fed surveys. Aim for $1,000 first, then 3-6 months' expenses.

How: Save $20-50/paycheck in a high-yield savings account (4-5% APY in 2025 via Ally or Capital One). Automate transfers post-payday.

Why it stresses less: It provides peace, reducing reliance on high-interest loans (average credit card APR 22%). 2025 data from NerdWallet shows emergency fund holders report 25% less financial anxiety.

Apply: Sell unused items on Facebook Marketplace for a boost—average $200-500. Story: Lisa, a waitress, saved $800 in six months by rounding up purchases, avoiding a payday loan when her car broke. What's your emergency fund status? Let's motivate each other in comments!

(Word count so far: 850)

Strategy 4: Master Grocery and Meal Planning—Stretch Your Food Dollar

Food costs eat 20-30% of low-income budgets, up 5% in 2025 per USDA. Smart planning can cut this by 25-40%.

Steps: Meal plan weekly, shop with a list, buy generics, and use apps like Flipp for coupons. Prep meals in batches to avoid takeout.

High-value hacks: Grow herbs at home (save $50/year), buy in bulk for staples, and use "no-spend" freezer weeks. Table of weekly meal plan example for $200/month (family of 4):

| Day | Breakfast | Lunch | Dinner | Snacks |

|---|---|---|---|---|

| Mon | Oatmeal | PB&J | Veggie stir-fry | Apples |

| Tue | Eggs | Leftovers | Bean soup | Carrots |

Story: The Smith family reduced food bills from $600 to $400/month by planning, freeing cash for debt. Engage: What's your go-to budget meal? Share recipes!

(Word count so far: 1050)

Strategy 5: Tackle Debt with Snowball or Avalanche Methods

Debt burdens low-income families, with average credit card debt $6,000 at 22% APR. Use snowball (smallest debts first for momentum) or avalanche (highest interest first for savings).

How: List debts, pay minimums, throw extra at one. In 2025, apps like Debt Payoff Planner automate this.

Why it works: Reduces interest paid, frees cash. CFPB data shows method users pay off 20% faster.

Apply: Negotiate rates (50% success). Story: Tom used avalanche to clear $4,000 in a year, reducing stress. Which method for you? Comment!

(Word count so far: 1200)

Strategy 6: Cut Utility and Housing Costs Creatively

Utilities average $300/month for low-income homes—cut 15-20% with habits like unplugging devices or sealing windows.

Steps: Switch to LED bulbs (save $75/year), use smart thermostats, or negotiate rent (success in tight markets).

High-value: Government programs like LIHEAP assist with energy bills. Story: A family saved $100/month by weatherproofing, building savings. Your utility hack? Share!

Strategy 7: Leverage Community Resources and Side Income

Don't go alone—use food banks, utility assistance, or community gardens to stretch budgets. For extra cash, gig apps like TaskRabbit add $200-500/month without full-time commitment.

Why: Builds resilience. 2025 data shows resource users save 10-15% on essentials.

Apply: Join local Facebook groups for free items. Story: Sarah used resources to save $150/month, starting a small home business. Your resource tip? Comment!

(Word count so far: 1400)

Strategy 8: Teach Kids Financial Literacy—Break the Cycle

Involve family in budgeting to foster habits. Use games like Monopoly or apps like Greenlight for allowances.

Why: Low-income kids often inherit struggles; early education changes that. Studies show financially literate youth save 20% more as adults.

Apply: Weekly family meetings. Story: A mom taught her kids tracking, now they save allowance. How do you teach kids money? Ideas welcome!

Strategy 9: Automate Savings and Expenses

Automation is magic for low-income budgets—set transfers to savings or bills to avoid late fees (average $30 each).

How: Use bank apps for direct deposit splits. In 2025, AI tools like Acorns round up purchases to save effortlessly.

Why: Builds habits without willpower. Users save 15% more.

Apply: Start with $10/paycheck. Story: A couple automated $50/month, building $1,200 in a year. Automated anything? Share!

(Word count so far: 1550)

Strategy 10: Seek Professional Help and Track Progress

Free credit counseling from NFCC or apps like YNAB provide plans. Track monthly with journals or spreadsheets.

Why: Accountability boosts success by 30%. 2025 resources include AI chatbots for advice.

Apply: Review quarterly, celebrate wins. Story: A family used counseling to cut debt 50%, stressing less. Your tracking method? Let's exchange tips!

Final Thoughts: Your Path to Financial Peace Starts Today

Smart budgeting for low-income families in 2025 is about empowerment—saving more, stressing less through these strategies. With economic trends like 3% growth and rising costs, these tips are lifesavers. Start small: Adopt one strategy today, like the 50/30/20 rule. Track progress, seek community, and watch your finances transform. Remember, consistency wins. What's your first step? Comment below—let's support each other on this journey to financial freedom! (Word count: 1650)

0 Comments